Porter's Five Forces for B2B SaaS

Porter's five forces still ask the right questions about your SaaS market. The problem is the answers change every quarter. Here's how to read each force for B2B SaaS in 2026, plus the sixth force Porter spent 30 years arguing about.

Contents

- The five forces still ask the right questions. In SaaS, the answers just expire.

- Threat of new entrants: the barrier moved from building the product to earning trust.

- Supplier power: your real suppliers are now your cloud bill and your model API.

- Buyer power: your buyer is drowning in tools and under orders to prune.

- Threat of substitutes: the scariest substitute is a prompt, a spreadsheet, or an internal build.

- Rivalry: feature parity now arrives in a quarter, not a product cycle.

- The piece Porter left out, and argued about for 30 years: complementors.

- The real problem isn't the forces. It's that you drew them once.

- How to actually run this

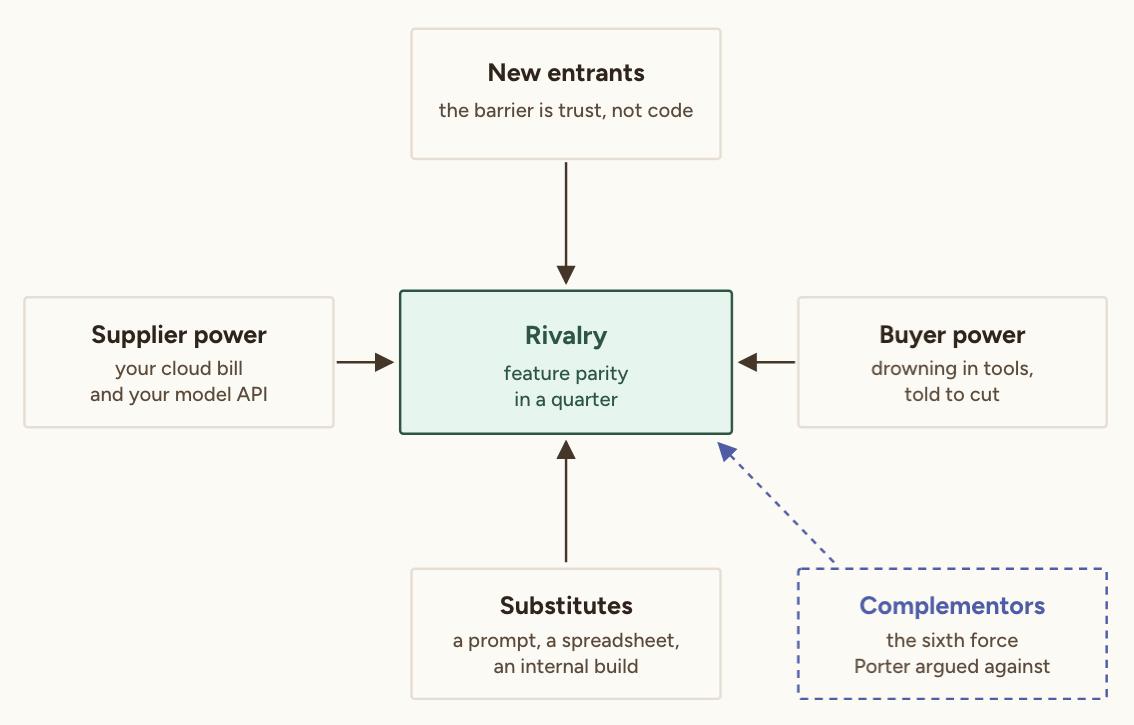

Porter's five forces (new entrants, supplier power, buyer power, substitutes, and rivalry) still ask the right questions about a B2B SaaS market. What breaks is the assumption underneath them: that industry structure holds still long enough to analyze. It doesn't in SaaS. A model release, a pricing change, or a funding round can flip a force in a quarter. So the framework is worth running, but run it as a standing question you re-answer, not a slide you fill in once. Below: each force framed for SaaS in 2026, the "sixth force" (complementors) that Porter rejected and Andy Grove didn't, and a worked example on a hypothetical company.

Michael Porter published the five forces in 1979, for industries that changed over decades: steel, autos, airlines. The model assumed industry structure was stable enough to map once and trust. B2B SaaS breaks that at the root, because a category can shift inside a single quarter, usually when you're not looking. That doesn't make the framework useless. It makes it a diagnostic you re-run, not a slide you fill in at the annual offsite and never touch again.

This is for the person doing the analysis, a product manager or marketer building a real competitive picture, not an MBA student filling in a template. We'll take each force in turn, translate it into SaaS terms with numbers instead of adjectives, then show what changes when you treat it as a live picture.

The five forces still ask the right questions. In SaaS, the answers just expire.

The framework itself is sound. Porter's insight, in the 1979 original and the 2008 update, is that an industry's profitability is set by five forces acting together, and that the strongest one or two matter most for strategy. Get the shape of all five right and you know where the profit pool sits and who's positioned to drain it.

Porter updated the model himself in 2008, and one change is telling: he expanded the entry-barrier list from six sources to seven, adding demand-side benefits of scale, his phrase for network effects. Even then the framework was straining to keep up with software, and it has strained harder since.

The failure mode isn't the five questions, it's the tense. Porter's model reads in the present simple, as if "supplier power is high" were a fact about your industry rather than a reading taken on a particular Tuesday. In a slow industry that's fine; the reading still holds a year later. In SaaS its half-life is weeks. Richard D'Aveni made the general case in 1994, in Hypercompetition: the snapshot is obsolete before the ink dries. So run each force, but treat every answer as a reading with an expiry date, not a fixed property of your market.

Threat of new entrants: the barrier moved from building the product to earning trust.

In SaaS, the cost of building has collapsed, so the barrier moved to everything that happens after the product works. Cloud infrastructure removed the capital requirement, off-the-shelf auth and payments and hosting removed most of the engineering, and AI coding tools removed much of what was left. A team that once needed a year and funding can ship a credible v1 in weeks.

So "can they build it" is no longer where the barrier lives. It moved downstream, to distribution, integration depth, and trust. A new entrant still has to land on your buyer's shortlist, integrate deep enough that ripping them out hurts, and clear procurement. Compliance is now a hard gate: most enterprise buyers won't sign without a SOC 2 report, which takes a newcomer months to earn. The reading to keep live isn't "how much data or funding do they have," it's "how painful are we to remove, and is that pain growing?"

Supplier power: your real suppliers are now your cloud bill and your model API.

For most SaaS companies the suppliers with real leverage aren't vendors in the traditional sense, they're the cloud and model providers you build on.

The model API is the clearest new case, and it cuts both ways. Supplier power there is low and falling: many providers, a running price war pushing model costs down, no single vendor cornering you. What hands power back is the lock-in around the model, not the model itself. Cloud providers charge you to move your data out, a switching cost scaled to what you've stored, so the more you build on one, the more it costs to leave.

Buyer power: your buyer is drowning in tools and under orders to prune.

Buyer power in SaaS is high and rising, driven less by classic buyer concentration and more by a buyer who already owns too many tools and has a mandate to cut. Procurement re-professionalized after the cheap-money era, and vendor consolidation is now an explicit target. You can see it in how contracts are written: Tropic's 2025 buying data shows 74.5% of contracts now run 13 to 24 months, up 56% year over year, as buyers trade flexibility for a negotiated price while trimming the vendor list. AI features are arriving with 20 to 37% price hikes at renewal, against a usual 3 to 9%, and buyers negotiate roughly 55% of that back down.

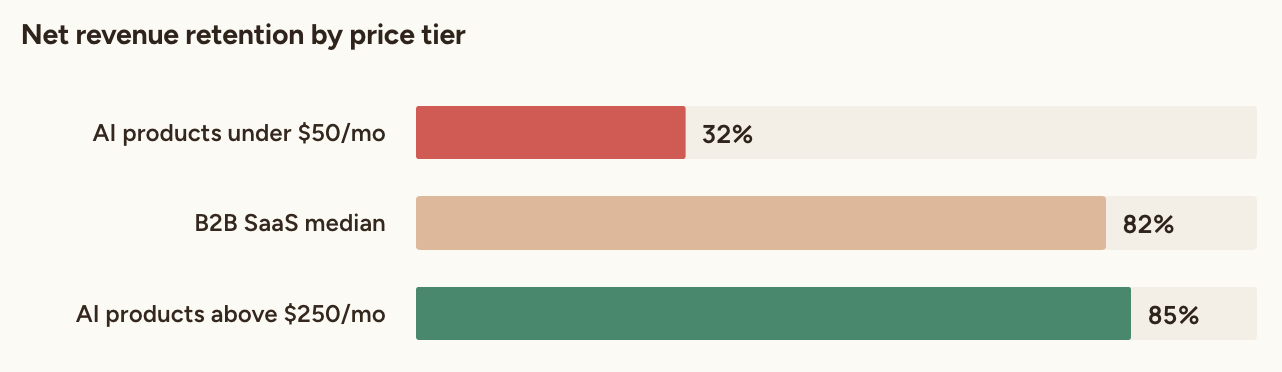

The self-serve norms of SaaS cut both ways. Free trials and month-to-month billing hand buyers an easy exit, capping your pricing power at the point of sale. The sharper signal is what happens after they buy, where retention splits hard by price. ChartMogul found low-priced AI tools churn brutally, with sub-$50-per-month AI products retaining at about 32% net revenue retention while AI products above $250 hold at roughly 85%, in line with the 82% median for B2B SaaS overall.

Cheap and easy to leave is a buyer-power problem. Embedded and worth keeping is a buyer-power defense. Are we getting more embedded in our buyers' workflows over time, or are we a line item waiting for the next consolidation review?

Threat of substitutes: the scariest substitute is a prompt, a spreadsheet, or an internal build.

In SaaS, the substitute that kills you usually isn't a rival product, it's the customer deciding they don't need one at all. Porter's substitute force asks what else solves the problem from outside your category. In software that's always included the spreadsheet, the general-purpose tool the team already pays for, and the "we'll just build it internally" impulse. AI sharpened all three and added a fourth: the agent that does most of the job from a prompt.

This stopped being theoretical in early 2026, when investors dumped SaaS stocks in a late-January selloff dubbed the "SaaS-pocalypse", fearing AI agents would substitute for whole categories of point-solution software. The market was pricing the substitute force in public.

The sober reads are more useful. Bain finds the most exposed tools are thin layers over a task an agent can just do, while incumbents that own a system of record are better placed to absorb agents than be replaced. Deloitte puts full application-layer replacement at least five years out, with agents mostly built on top of systems of record for now. So the uncomfortable question: if a competent agent had your customer's data, how much of what you charge for could it just do, and what's left that it can't?

Rivalry: feature parity now arrives in a quarter, not a product cycle.

Rivalry in SaaS is structurally brutal, because categories tend toward oligopoly and features copy fast. Jason Lemkin argues at SaaStr that SaaS markets settle into a handful of viable competitors, because high development cost plus a small initial market only supports a few players at efficient scale, and once a leader emerges, competition hardens into a fight for the same accounts.

Anything worth copying gets copied, and the copy cycle keeps shortening, because the same AI tools lowering entry barriers let rivals match a feature soon after you announce it. That's why the feature checklist is a losing game in most categories. The reading worth keeping live isn't "who has which features," because that table is stale the week you build it. It's "where are rivals moving," on pricing, positioning, and which segment they're chasing, because those moves tell you where the next fight is before it shows up in a lost deal.

The piece Porter left out, and argued about for 30 years: complementors.

The force that matters most for platform-era SaaS, complementors, is the one Porter deliberately kept out of the model. A complementor is a company whose product makes yours more valuable: your Slack app, your Salesforce integration, the marketplace you list in. Not your supplier, buyer, or rival, and in SaaS often the difference between distribution and obscurity.

The history is worth getting right, because most posts get it wrong. Andy Grove coined "six forces" in Only the Paranoid Survive (1996), bolting complementors onto Porter's five. Adam Brandenburger and Barry Nalebuff introduced complementors and the value-net model earlier, in a 1995 HBR article and the 1996 book Co-opetition, but by their own 2024 paper they'd never formally called it a force. And Porter rejected the promotion in 2008, arguing complements shape profitability through the existing five rather than acting as a sixth.

You don't need to settle the argument, just to notice that a force acts on your SaaS business that the classic five don't name, and in the platform economy it's often the strongest one. The 2016 HBR piece on platforms put it plainly: the five-forces model "describes competition among traditional 'pipeline' businesses." It wasn't built for platforms, where outside players and network effects add value rather than extract it, exactly what complementors do. If a real share of your growth runs through another company's ecosystem, you're working a value net, not a value chain.

The real problem isn't the forces. It's that you drew them once.

Every reading above expires, so the framework only works as a live picture you refresh, not a slide you archive. Run the five forces (plus complementors) as a standing set of questions, and the value isn't the snapshot, it's noticing the moment an answer changes.

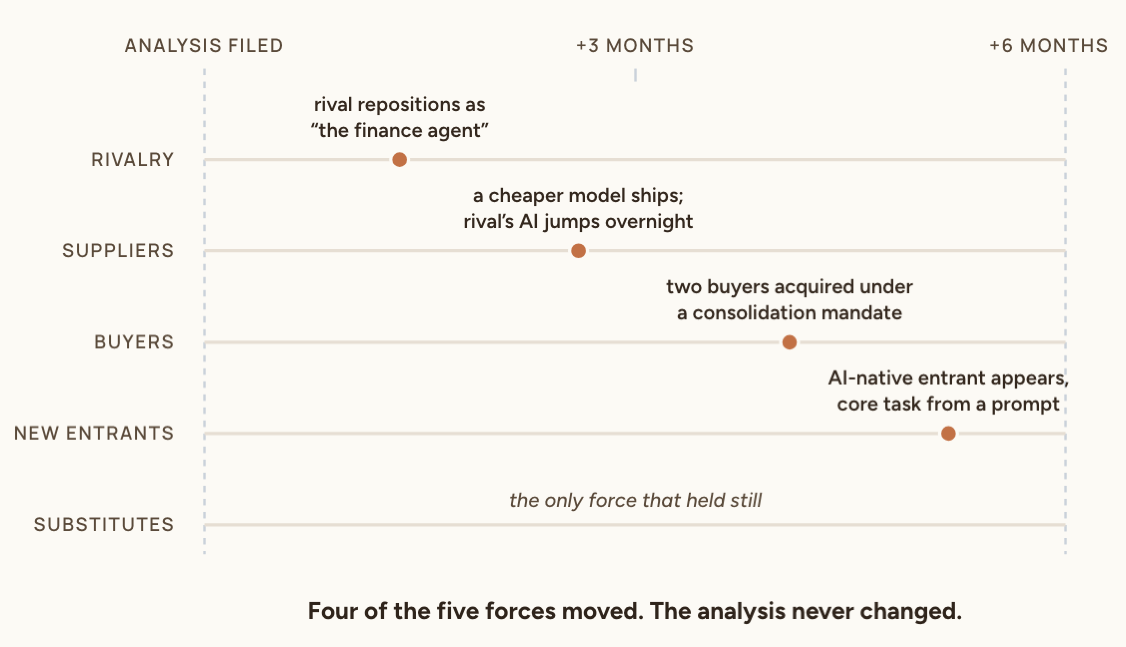

Picture a 30-person B2B SaaS automating accounts-payable for mid-market finance teams. The day they run the analysis, the picture looks stable: three familiar rivals, moderate buyer power because switching AP tools mid-year is a hassle, distant substitutes, suppliers that are just the cloud bill. They write it up, feel informed, and file it.

Now watch the forces move over two quarters, none of it visible in that filed document. A rival raises a round and repositions from "AP automation" to "the finance agent," a substitute-force shift disguised as rivalry that reframes the category. A model provider ships a cheaper, better model and the rival's AI features improve overnight, a supplier move flowing straight into rivalry. Two target buyers get acquired by a parent with a consolidation mandate, so buyer power jumps for a whole segment. An AI-native entrant appears that does the core task from a prompt. Four of the five forces moved in six months. The filed analysis describes a company that no longer exists.

The fix isn't a better template, it's a shorter loop. Connect the five-forces picture to what your competitors and market do week to week, so the funding round, the repositioning, the pricing change, and the new entrant land as signals you catch, not surprises you reconstruct in a post-mortem. That's why we built meertrack: it watches competitor pricing, product updates, hiring, and messaging, filters the noise with AI, and sends what matters to Slack, so your inputs stay current instead of stale in a doc. It runs $19 per competitor per month, against the $10K to $40K a year enterprise CI tools charge, and you don't need many (a short list of the competitors who actually show up in your deals is enough). The framework tells you which changes matter. Monitoring tells you when they happen.

How to actually run this

Run the five-forces pass this week, with numbers where you have them and question marks where you don't, and add complementors if real growth runs through another company's ecosystem. Then write down the two or three readings that would flip your strategy, and put something in place to catch them. The analysis is worth an afternoon. Keeping it true is worth more, the part Porter's 1979 world never had to solve.